26/10/2020

Flash boursier

Key data

| USD/CHF | EUR/CHF | SMI | EURO STOXX 50 | DAX 30 | CAC 40 | FTSE 100 | S&P 500 | NASDAQ | NIKKEI | MSCI Emerging MArkets | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Latest | 0.90 | 1.07 | 10'023.90 | 3'198.86 | 12'645.75 | 4'909.64 | 5'935.98 | 3'465.39 | 11'548.28 | 23'516.59 | 1'136.45 |

| Trend | |||||||||||

| %YTD | -6.43% | -1.18% | -5.59% | -14.59% | -4.55% | -17.87% | -21.30% | 7.26% | 28.71% | -0.59% | 1.95% |

Highlights:

1. Surge in virus cases stokes fears

2. Chinese exports and industrial production on the rise

Business shutdowns and surging virus cases rattle investors

Core equity markets staged corrections last week, pulled down by concerns about the continuing pandemic and the renewed restrictions on business introduced in several European countries. A curfew was introduced in Spain and Italy, forcing bars and restaurants to close early. In the US, the number of daily cases skyrocketed over the weekend to upwards of 83,000, with a sharp increase in the less populated areas spared during the first wave.

Mild anxiety over the outcome of the presidential election is stoking volatility because of the implications for investors, particularly with regard to corporate taxation. The final televised debate between the two candidates was not particularly revealing with regard to their respective economic platforms. However, in the wake of his performance, Joe Biden is tipped to win. He remains ahead in the polls at 51.4% of the vote, even though the gap relative to Donald Trump (42.7%) has narrowed. Whichever man is chosen to be president, a bumper stimulus package is likely to be forthcoming. But should Joe Biden win the presidential election and the Democrats also secure a Senate majority, tax hikes could ensue, which could then hurt businesses.

Fears of recession in the third quarter in Europe are gathering pace according to recent business surveys. The services PMI fell sharply in France (46.5). In contrast, in Germany, the manufacturing PMI recovered to 58. Christine Lagarde, who heads up the ECB, which meets this Thursday, last week reiterated that the ECB remains ready to use all instruments at its disposal to support the economy. However, the market believes that no concrete measures will be announced before the December meeting. In the meantime, China’s economy continues to recuperate, boasting a sharp increase in exports and industrial production (+6.9% year-on-year in September). Chinese equities are likely to continue performing positively, especially as their weighting in world indices is increasing.

Generally speaking, corporate results in the US have not been as bad as expected, with earnings largely beating expectations. Financials reported by tech giants (Amazon, Apple and Alphabet) after the closing bell this Thursday are to be watched closely.

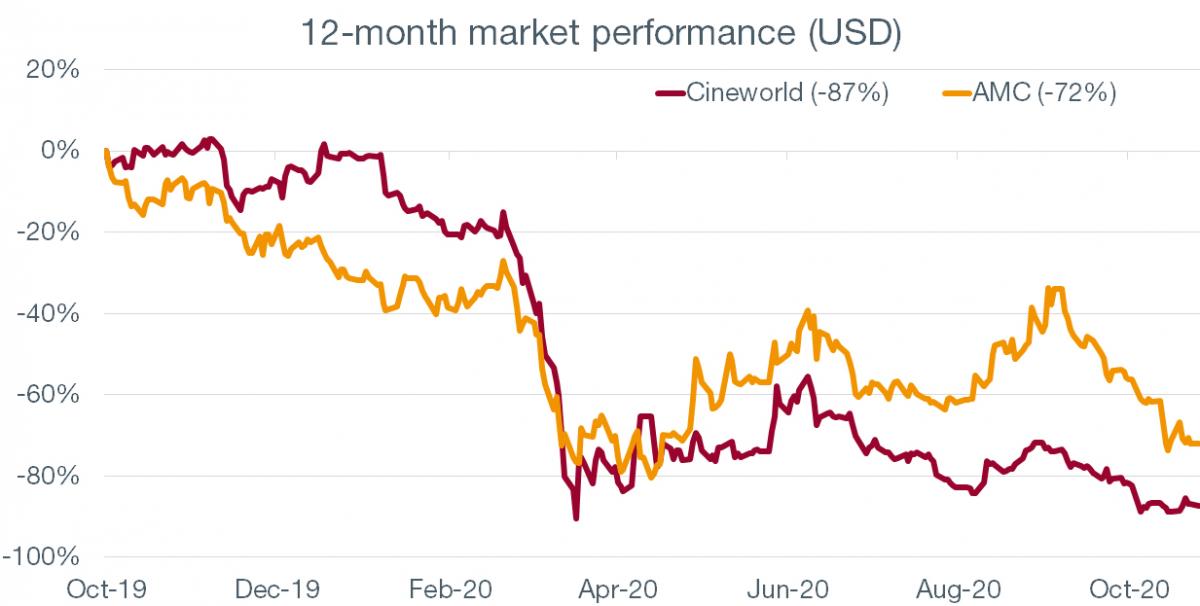

Lethal intermission

The pandemic is making life hard for cinemas. On 9 October, Cineworld, the world’s second-largest cinema chain (after AMC), temporarily shut its 536 cinemas in the US (and 127 locations in the UK) after the release of several blockbusters, such as the latest James Bond movie, was postponed. This final outing for Daniel Craig as 007 was due for release in the first quarter of 2020. It was then postponed to November this year. It will finally be released in March 2021.

In the face of the pandemic, film studios have three choices: screen a film in near-empty cinemas, release the film directly to streaming platforms, leading to much smaller returns, or postpone the release outright. MGM, the studio that produced the latest James Bond film, has chosen the last option. And it is a lethal choice for cinema owners, who now find themselves with no material and no customers.

In addition, giants such as Cineworld and AMC have invested heavily (by taking out large loans) to give customers an attractive alternative to evenings spent at home watching Netflix. As a result, they are now heavily indebted, facing paltry revenues and a stockmarket price that has been decimated, to the point where Moody’s is not ruling out bankruptcy..