11/01/2021

Flash boursier

Key data

| USD/CHF | EUR/CHF | SMI | EURO STOXX 50 | DAX 30 | CAC 40 | FTSE 100 | S&P 500 | NASDAQ | NIKKEI | MSCI Emerging MArkets | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Latest | 0.89 | 1.08 | 10'797.99 | 3'645.05 | 14'049.53 | 5'706.88 | 6'873.26 | 3'824.68 | 13'201.98 | 28'139.03 | 1'353.53 |

| Trend | |||||||||||

| %YTD | 0.05% | 0.06% | 0.88% | 2.60% | 2.41% | 2.80% | 6.39% | 1.83% | 2.43% | 2.53% | 4.82% |

Highlights:

1. Markets still in fine fettle

2. Investors upbeat about future

Fiscal stimulus, vaccines and heady markets

Global stock exchanges set more records in the first week of 2021, led by emerging economies. Meanwhile, the virus is proving hard to handle as it seems to be spreading ever more quickly. All eyes are riveted on political happenings in the US and progress in European vaccination campaigns. Democratic congressmen are furthermore expected to launch impeachment proceedings against President Trump, citing charges of ‘inciting insurrection’, less than a fortnight before his term expires.

Central banks are active on the markets like never before, representing global liquidity of some USD 1 trillion. This news, combined with the prospect of wider vaccination and fiscal splurges from governments, is cheering investors – who are looking to the future with a fair deal of optimism. Despite weak economic data out of the US and the unprecedented civil insurrection in Washington DC, equity markets are heading firmly upwards. Investors are also expecting a larger dose of stimulus now that Congress is fully under the control of the Democrats and will thus dance to Joe Biden’s tune. For one, we can expect higher corporation taxes, beefed-up capital gains tax together with tighter industry regulations. But bear in mind that the midterm elections are only two years away, and voters will not look kindly upon dogmatic far-left policies. Expect therefore more moderate measures than might otherwise be possible. On international trade, the arrival of Janet Yellen at the Treasury is positive. Tensions between China and the US are also expected to be dialled down.

Leading stocks higher last week were cyclicals and financials, in response to stronger bond yields, the prospect of extra fiscal stimulus and hence a better economic recovery. The trend has been particularly positive for mining stocks, which are benefiting from both China’s ongoing recovery and the weak dollar.

US job figures for December disappointed, showing that 140,000 jobs had been lost, but investors shrugged off the news. The rise in Covid-19 cases and efforts to contain the pandemic dented the travel & leisure and hospitality sectors. The unemployment rate was unchanged at 6.7%. The 0.8% increase in hourly wages represented some unexpected good news. Employment figures for previous months were revised upwards sharply.

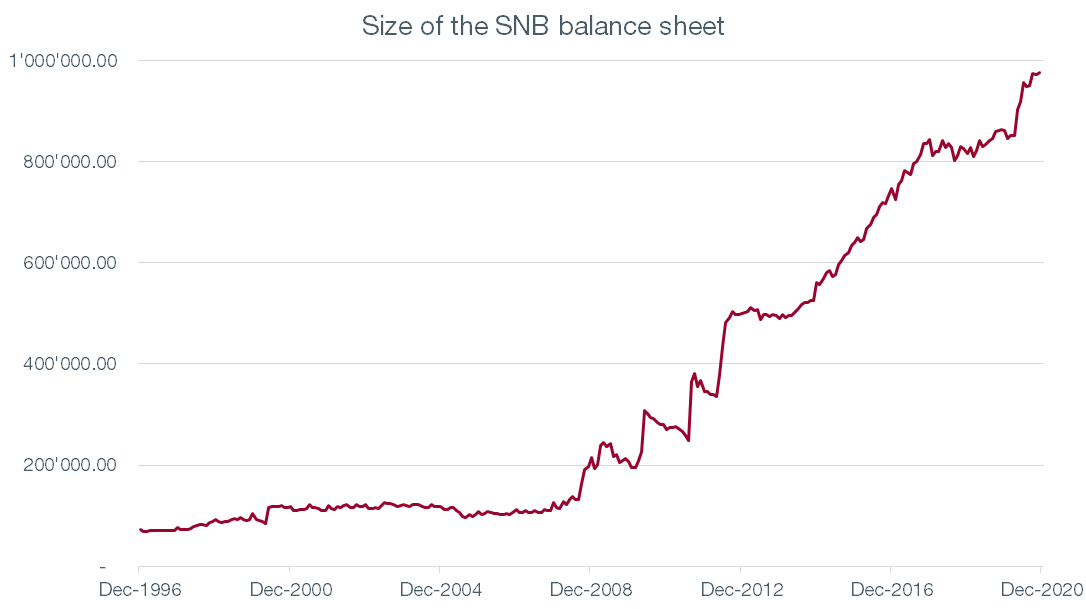

SNB reports bumper profits in 2020

The SNB has reported profits for 2020, which amounted to CHF 21 billion. This huge figure was mainly the result of positions in foreign currencies and gold, which has continued to serve as a safe haven as central bank have operated their printing presses at full tilt and the US government has enacted strong doses of fiscal stimulus.

This windfall will enable the SNB to distribute CHF 4 billion to the Confederation and cantons. The dividend for private shareholders will amount to CHF 15 per share. Its foreign currency reserves continue to swell as it strives to contain the strength of the Swiss franc.

In 2020, for the first time in its history, the SNB’s interventions in the foreign exchange market earned it the moniker of ‘currency manipulator’ from the US Treasury. The balance sheet now stands at around CHF 700 billion, representing three-quarters of Swiss GDP. On the basis of the total assets/GDP ratio, this places Switzerland ahead of the US and the European Union, which have ratios of 30% and 60%, respectively.